The story of Black-owned dealerships is not just a story about selling cars. It is a story about who gets trusted with capital, territory, inventory and the right to represent an American brand.

The story of Black-owned dealerships is not just a story about selling cars. It is a story about who gets trusted with capital, territory, inventory and the right to represent an American brand.

By KOLUMN Magazine

The American car dealership has always sold more than transportation. It sells arrival. It sells status. It sells suburban possibility, family safety, business credibility, Saturday freedom and the fantasy that the open road belongs equally to everyone. But for Black Americans, the dealership has never been merely a showroom with glass walls and polished floors. It has also been a gatekeeping institution, a credit desk, a negotiation theater and, for the very few who managed to own one, a rare command post inside one of the most capital-intensive corners of American commerce.

That is why the legacy of Black-owned car dealerships cannot be measured only by the number of vehicles sold or the size of annual revenues. It has to be understood as part of a larger Black business history, one that KOLUMN has explored in stories about minority business infrastructure, Black consumer power and C.R. Patterson & Sons, the Ohio carriage-and-automobile firm remembered by the Smithsonian’s National Museum of African American History and Culture as the only African American owned and operated automobile company. The dealership is where those themes converge: manufacturing history, migration, credit, entrepreneurship, discrimination, consumer dignity and the politics of who is trusted to move metal at scale.

The current landscape is both impressive and stark. According to reporting drawing on National Automobile Dealers Association and National Association of Minority Automobile Dealers figures, there are roughly 266 Black-owned car dealerships in the United States, a number that remains tiny when measured against an industry of more than 18,000 dealership rooftops. Urban Science reported that the U.S. dealership count stood at 18,374 rooftops at the end of 2024, while NAMAD says that minority consumers purchase about 32 percent of all new vehicles even though only a small share of dealerships are minority-owned. That imbalance is not incidental. It is the residue of a century of exclusion from franchise rights, bank financing, floorplan credit, manufacturer confidence and succession capital.

The paradox is that Black consumers have long been essential to the automobile market while Black dealers have remained exceptional inside it. Cars shaped the Great Migration, opened routes between Southern hometowns and Northern factories, carried domestic workers across segregated geographies, made the Green Book necessary, and helped Black families build modern lives around mobility even when housing, schooling and employment were constrained by segregation. Yet the business of retailing new cars — the franchise, the service department, the finance-and-insurance office, the warranty relationship, the manufacturer allocation pipeline — remained mostly outside Black ownership.

Before the Franchise, There Was Patterson

The historiography of Black automotive enterprise usually begins not in Detroit, but in Greenfield, Ohio, with C.R. Patterson & Sons. The company moved from carriage building into automobile production in the early twentieth century, and the Smithsonian notes that Patterson-Greenfield automobiles were produced from 1915 to 1918. No known Patterson-Greenfield automobile survives, which gives the story a ghostly quality: an enterprise consequential enough to belong in the national record, yet materially absent from the museums and private collections that preserve so many white-owned automotive relics.

That absence matters. Automotive history is often narrated through factories, inventors and brands, but Black automotive history is also a history of disappearance. Companies are remembered in fragments. Dealers are remembered in trade lists. Pioneers appear in anniversary articles, then vanish from mainstream business memory. The result is a public imagination in which Black people are seen as drivers, workers, consumers and cultural stylists of the automobile, but less often as owners of the commercial systems that sell, finance and service it.

Patterson complicates that erasure. It shows that Black ownership was present at the dawn of the automobile age, not as a symbolic afterthought but as a working business with manufacturing competence, skilled labor and regional ambition. It also shows how brutal the transition from carriage to car could be for any small firm, especially one trying to compete in an industry quickly consolidating around scale, capital and production systems that favored giants.

Homer Roberts and the Franchise Door

If Patterson represents the manufacturing origin, Homer B. Roberts represents the franchise breakthrough. In 1923, Roberts was awarded a Hupmobile franchise in Kansas City, Missouri, a milestone preserved in the African-American Automobile New Car Dealers historical timeline as the moment when he became the first African American franchised as a new-car dealer. Roberts was not merely a businessman who happened to sell cars. He was a sophisticated operator who understood that Black buyers were being ignored by white dealerships and that the automobile had become an instrument of modern citizenship.

Roberts built a sales force that included Black salesmen and cultivated Black professionals, churches and civic networks. His achievement should be read within the context of Jim Crow capitalism, where Black entrepreneurs often had to create parallel institutions because mainstream institutions either excluded Black customers or treated them as marginal. In that world, a Black dealership was not only a retail outlet; it was a statement that Black consumers deserved professionalism, courtesy and access to new technology.

The Roberts story also reveals an enduring pattern. Black dealers have often entered the industry by proving the value of customers whom the wider market underestimated. They did not simply ask manufacturers for inclusion on moral grounds. They demonstrated that Black markets were profitable, loyal and strategically important. Their burden was double: sell cars and prove that Black demand existed, even when Black people had already been buying cars for decades.

Ed Davis and the Detroit Breakthrough

For many historians of Black auto retail, Edward Davis remains the central figure. Born in Shreveport in 1911 and raised in Detroit, Davis entered the car business when the industry’s employment and ownership ladders were sharply segregated. The Detroit Historical Society identifies him as the first African American owner of a new car dealership in the United States, noting that Studebaker offered him a franchise in 1940 after recognizing his success selling to Detroit’s Black population. The Automotive Hall of Fame similarly records that Davis opened Davis Motor Sales in 1938 and received the Studebaker franchise in 1940.

Davis’s career has to be placed inside Detroit’s Black geography. Paradise Valley and Black Bottom were not simply neighborhoods; they were dense worlds of enterprise, nightlife, labor, church life and political organizing. A Black dealership operating there did more than move inventory. It helped anchor a commercial ecosystem. It gave Black buyers a place to be treated as primary customers. It employed people. It circulated money. It supplied a form of business visibility that mattered in a city whose factories depended on Black labor but whose corporate offices rarely imagined Black authority.

His story also carries the violence of urban redevelopment. The Detroit Historical Society notes that the construction of I-75 through Davis’s Paradise Valley property contributed to the closure of his business in 1962, a detail that links Black auto retail to the broader history of highway destruction in Black neighborhoods. The irony is difficult to miss. Federal and local highway policy helped create the automobile-dependent metropolis while also cutting through the very Black commercial districts where automotive entrepreneurship had taken root.

Davis returned with another breakthrough. In the early 1960s, he secured a Chrysler-Plymouth franchise, becoming the first African American to receive a Big Three franchise. His dealership reportedly prospered, selling about 1,000 new cars annually and twice as many used cars, according to the Detroit Historical Society. That success should have opened the floodgates. Instead, it became a celebrated exception.

The Capital Wall

The modern dealership is not a small business in the romantic sense. It is a high-risk, high-capital enterprise built on real estate, inventory financing, manufacturer approval, working capital, facility requirements, service equipment, payroll, insurance, compliance systems and the ability to withstand market shocks. A dealer may be locally known, but the business itself sits inside a national structure of franchise law, manufacturer relations and lender confidence.

That structure has never been race-neutral. NAMAD says its work includes advocating before manufacturers and policymakers to increase the number of minority-owned dealerships and protect ethnic minority dealer interests. Its own public framing points to the central contradiction: minorities buy a large share of new vehicles, but minority ownership remains disproportionately small. The organization also notes that 95 percent of minority dealers are first-generation owners, a statistic that explains much of the fragility. First-generation ownership means fewer inherited rooftops, fewer family balance sheets, fewer intergenerational banking relationships and fewer internal succession pipelines.

Black Enterprise has long treated auto retail as one of the major arenas of Black business scale. Its Auto 40 rankings include dealer groups with hundreds of millions, and in some cases billions, in revenue. The presence of firms like RLJ McLarty Landers, Wade Ford and other large Black-owned dealer groups proves that Black operators can compete at the highest levels of automotive retail. But the rankings also reveal how concentrated success is. There are major players, and then there is a long, difficult gap between aspiration and acquisition.

Damon Lester, former president of NAMAD, has been especially direct about the constraints. In a Black Enterprise report on the largest Black auto dealers, Lester identified insufficient capital for acquisitions and weak succession planning as major challenges, while noting that the average Black dealer was about 60 years old. That observation should be read as both a warning and a succession map. If the next generation cannot access capital, buy stores, inherit stores or partner with manufacturers on favorable terms, the number of Black-owned dealerships can decline even while the industry remains profitable.

The Customer Side of the Ledger

Any honest account of Black-owned dealerships must also confront the consumer experience that makes them necessary. For generations, Black car buyers have faced discrimination not only in whether they were welcomed into showrooms, but in the terms they were offered after they arrived. The Consumer Financial Protection Bureau and Department of Justice ordered Ally Financial to pay $80 million to consumers after determining that more than 235,000 minority borrowers paid higher interest rates on auto loans between 2011 and 2013. The National Consumer Law Center has similarly argued that discretionary dealer markups have produced racial disparities, noting that African American borrowers were more likely to have loans marked up and paid higher markups than white borrowers in litigation data reviewed by advocates.

More recent enforcement actions show that the problem has not vanished. In 2024, Reuters reported that the Federal Trade Commission sued Asbury Automotive Group, alleging that three Texas dealerships charged Black and Latino customers more for the same add-on products and added services without consent; Asbury denied the allegations and said it would fight the case. The FTC alleged that Black customers paid an average of $298 more and Latino customers $214 more for the same add-ons than white customers who were not Latino.

The point is not that Black-owned dealerships are automatically virtuous or that ownership alone solves every consumer protection issue. Journalism should resist that simplification. Dealers of all backgrounds operate within a profit-driven industry, and consumers can face opaque pricing, extended warranty pressure, negative equity traps and financing confusion anywhere. But ownership matters because institutional culture matters. Representation at the dealer-principal level can shape hiring, community outreach, customer respect, language access, financial education and whether a dealership sees Black buyers as targets to be extracted from or relationships to be cultivated.

That distinction has become even more important as consumer protections have become politically contested. The FTC announced its Combating Auto Retail Scams Rule in 2023 as a way to fight junk fees and deceptive practices in vehicle shopping, saying it would prohibit certain exploitative fees and require clearer pricing. But in January 2025, Reuters reported that a federal appeals court threw out the rule on procedural grounds after a challenge by dealer groups. For Black consumers, who have long faced discriminatory treatment in auto finance, the weakening or delay of transparency rules is not an abstract regulatory matter. It affects the price of mobility.

Women, Legacy and the Second Generation

The Black dealership story is also increasingly a story about women and succession. Bob Ross Buick GMC in Ohio traces its roots to 1979, when Bob Ross acquired what became a landmark Black-owned dealership. After his death, Norma Ross took over, and later Jenell Ross continued the family legacy. The dealership describes itself as one of the country’s few Black- and woman-owned dealerships and identifies Jenell Ross as a second-generation African American female auto dealer. Her presence matters because the industry’s ownership ranks have historically been overwhelmingly male, and Black women have faced the compounded barriers of race, gender and capital access.

The Ross legacy also shows why succession planning is not a bureaucratic detail. In many Black businesses, survival across generations is the difference between a breakthrough and an institution. A founder may fight through the first gate, but without estate planning, manufacturer approval, management training and acquisition capital, the business can disappear when the founder retires or dies. The next generation must inherit not only the name, but the operating capacity.

NAMAD’s NextGen program speaks directly to that challenge by trying to connect emerging dealership leaders with resources, people and ideas. That kind of pipeline work is not glamorous, but it is existential. The future of Black auto retail will depend less on ceremonial diversity statements than on whether younger operators can get trained, financed and approved to own rooftops.

Electric Vehicles and the Next Gate

The transition to electric vehicles may become the next great test. EVs are not simply new products; they change service revenue, technician training, facility investments, charging infrastructure, customer education and manufacturer strategy. For dealers with deep capital reserves, the transition is difficult but manageable. For undercapitalized dealers, it can become another gate.

Manufacturers are asking dealers to invest in chargers, tools, facility upgrades and training at the same time that the economics of EV adoption remain uneven across regions and income groups. Black-owned dealerships may find opportunity in becoming trusted EV educators in communities often excluded from early infrastructure investment. But they may also face the risk of being squeezed if facility mandates and brand requirements become too expensive.

This is where public policy, manufacturer commitment and private capital intersect. If the EV transition is treated only as a technology story, it will reproduce older inequalities under a greener banner. If it is treated as an ownership story, it could become a rare chance to expand Black participation in the next era of automotive retail.

What the Road Ahead Requires

The future of Black-owned dealerships will not be secured by nostalgia. Celebrating Patterson, Roberts and Davis is necessary, but commemoration without capital is a dead end. The industry needs measurable commitments: more manufacturer-backed acquisition pathways, stronger floorplan financing access, transparent franchise approval processes, formal succession partnerships, EV transition grants, and dealer-development programs with actual rooftops at the end of the pipeline.

It also requires a broader public understanding of what is at stake. A dealership is not just a place to buy a car. It is a local employer, a tax generator, a service center, a lender-facing institution, a sponsor of Little League teams and scholarship breakfasts, a commercial landholder and a visible claim on the American marketplace. When Black people own dealerships, they own part of the machinery through which mobility is priced and distributed.

The old promise of the automobile was freedom. But freedom has always depended on who controls the keys, who writes the loan, who owns the lot and who gets to stand behind the glass doors as principal rather than petitioner. Black-owned dealerships have spent a century proving that Black enterprise belongs not at the margins of the American road, but at its center. The remaining question is whether the industry will finally treat that proof as a beginning, not an exception.

More great stories

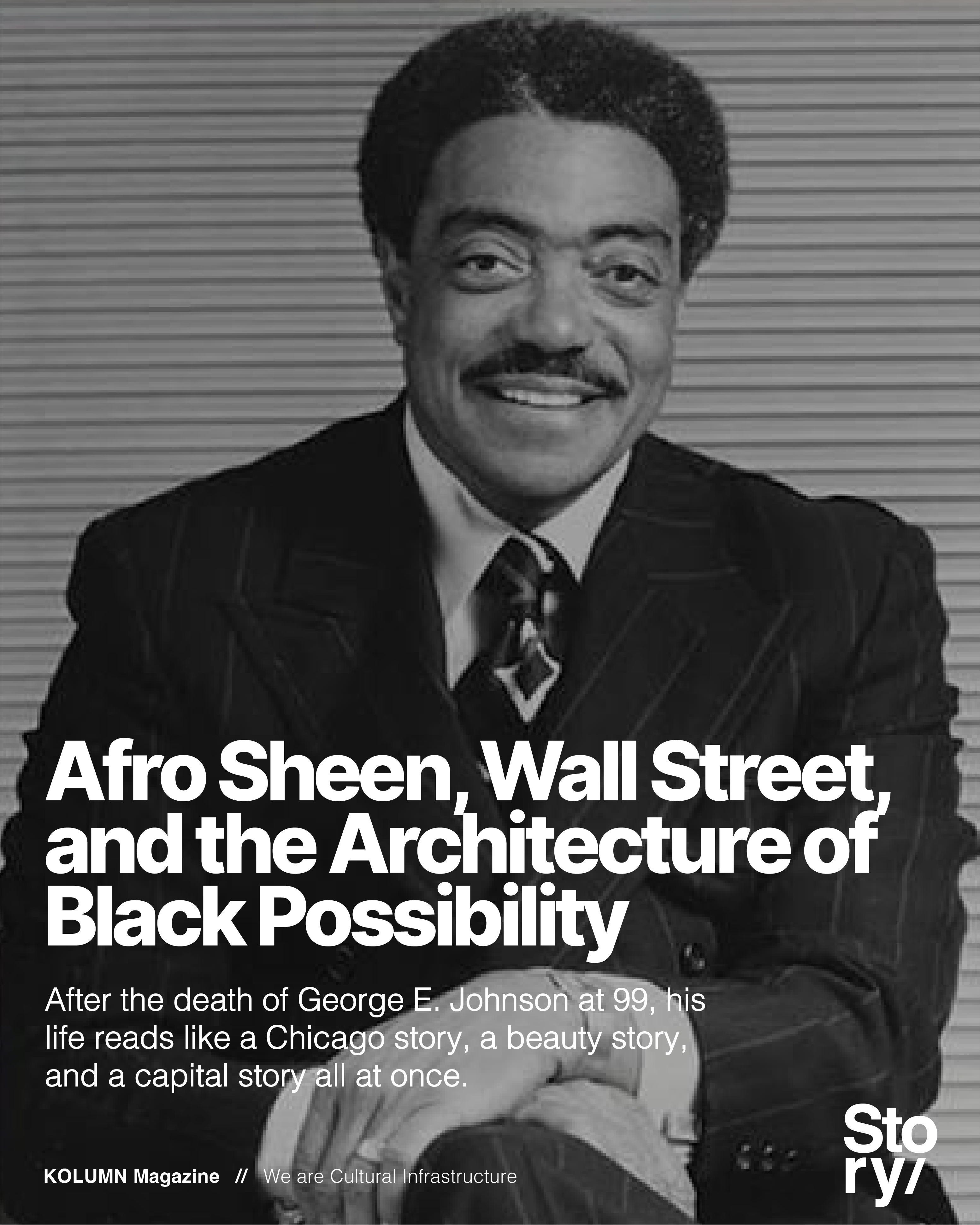

Afro Sheen, Wall Street, and the Architecture of Black Possibility

July 6, 2026

No Comments

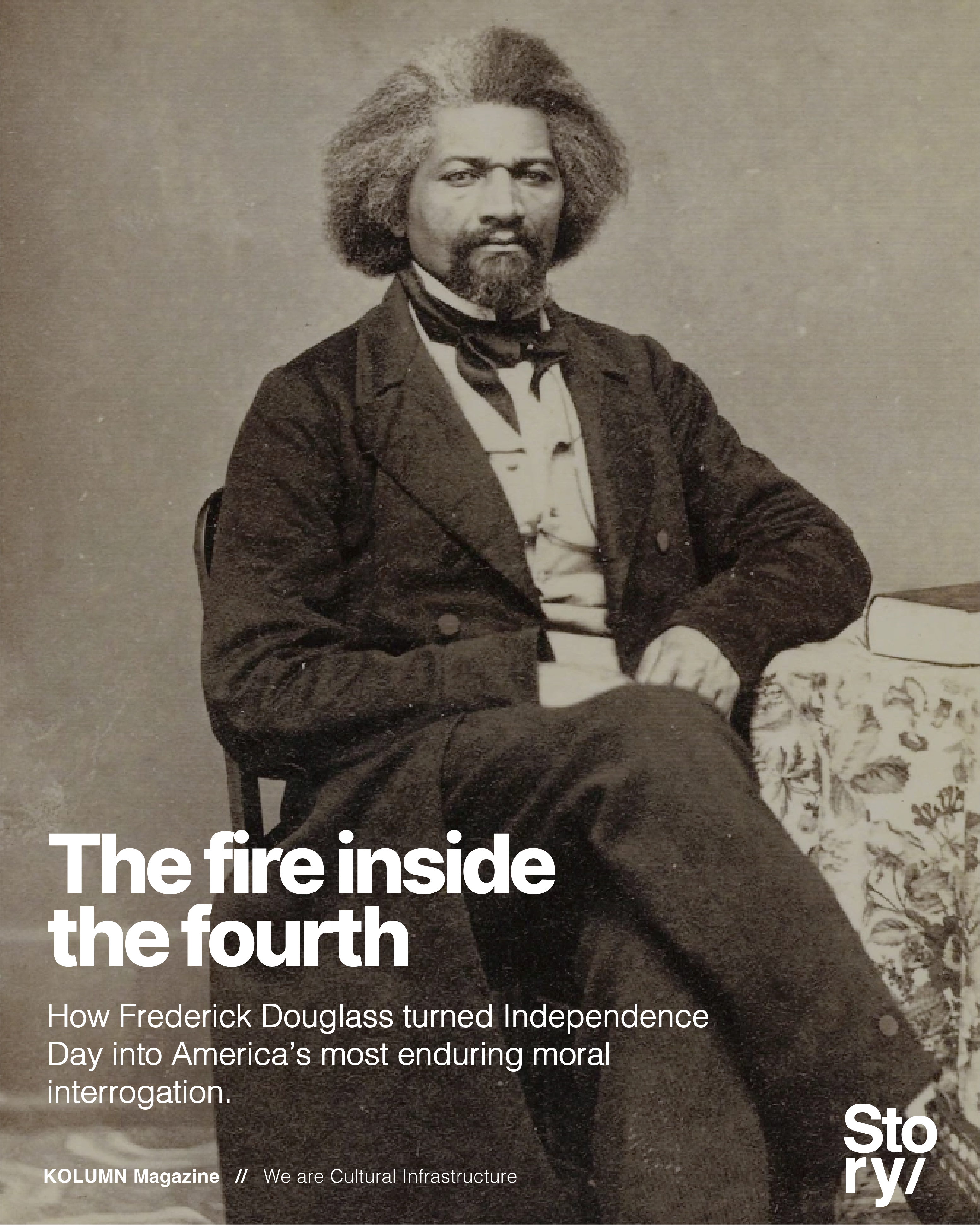

The Fire Inside the Fourth

July 5, 2026

No Comments