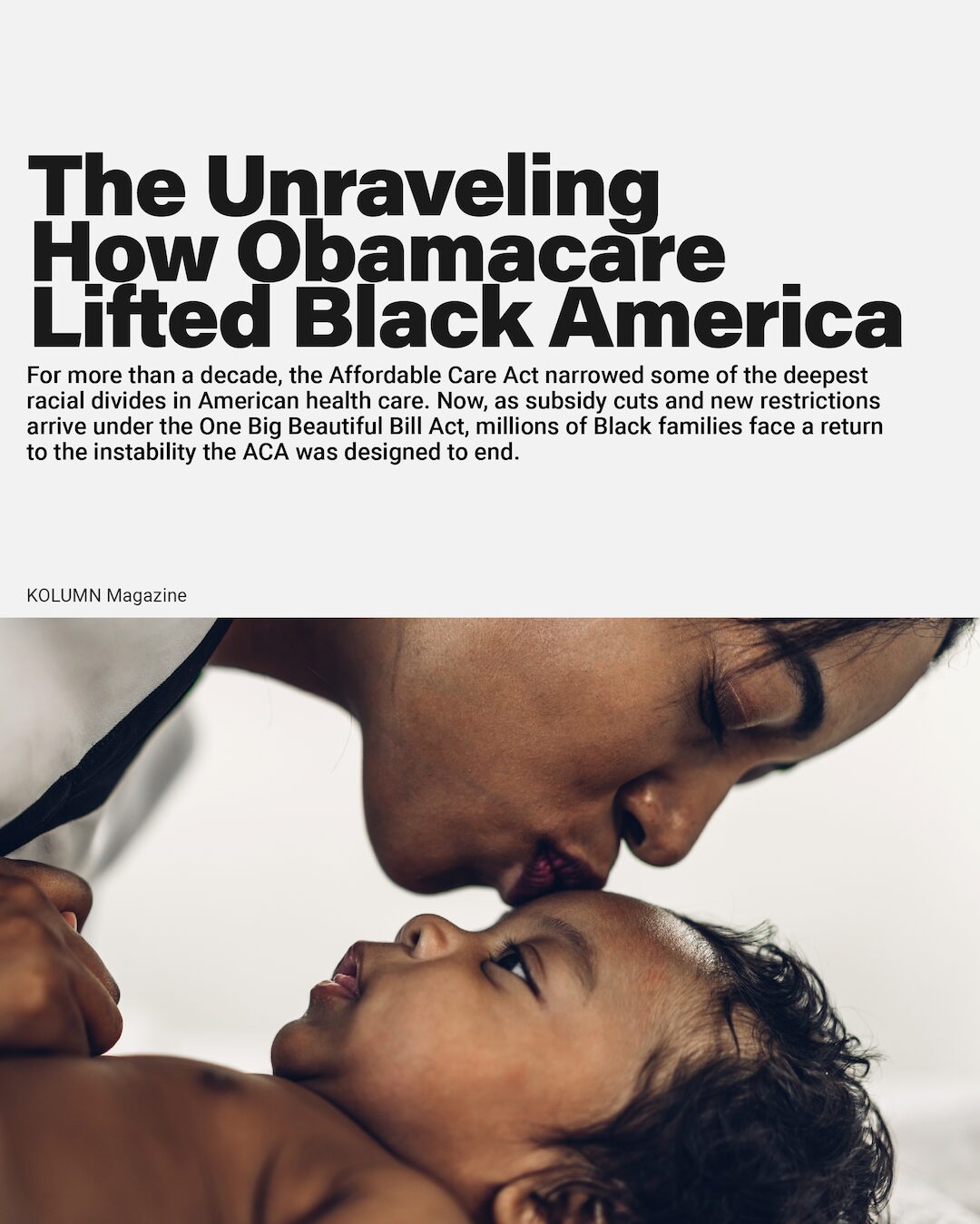

The Unraveling

How Obamacare Lifted Black America—And Why a New Law Threatens to Pull It Apart

By KOLUMN Magazine

On a gray Tuesday morning in Atlanta, the lobby of a community health clinic feels strangely like the waiting area of a neighborhood bank. People arrive with folders of financial documents—pay stubs, tax returns, letters from insurers—waiting not for medical procedures but for explanations: what their premiums will be next year, whether their subsidies will survive, what the shifting rules of the Affordable Care Act now mean for their families.

Near the intake desk, a mortgage underwriter named Monique sits with her paperwork neatly clipped together. At work she evaluates other people’s financial risk; lately, she says, “it feels like someone’s underwriting me.” For the past four years, the ACA’s enhanced subsidies have kept her family’s health insurance within reach—$90 a month for a silver plan that covers her husband, a contract worker, and their two children, both of whom have asthma.

I approve loans for people ruined by medical bills,” Monique said. “Now I’m the one who might lose coverage.”

Then came the notice. If Congress fails to extend the enhanced subsidies that were expanded during the pandemic and are set to expire at the end of 2025, her premiums could more than double. Combined with the new restrictions and administrative hurdles created by the One Big Beautiful Bill Act, signed by President Donald Trump on July 4, 2025, the future of her family’s coverage feels suddenly unstable.

For millions of Black Americans, the ACA was not simply a policy achievement—it was a rare correction in the long, uneven history of American health care, a system that has always asked Black families to sacrifice more, wait longer, and accept less. It is also, now, a reminder of how fragile political wins can be.

The World Before Obamacare

When President Barack Obama signed the Affordable Care Act into law in 2010, it entered a country stratified not only by class and geography but by race. The health system, even in its most routine functions, divided Americans along fault lines that were as old as the nation itself.

The ACA didn’t fix everything, but it gave us room to breathe,” a Detroit caterer told me. “Losing it feels like the air closing in.

Black Americans were more likely to work in jobs without employer-based insurance—retail, care work, transportation—and more likely to experience lapses in coverage when those jobs ended. They were also more likely to be uninsured in the first place. Before the ACA’s central provisions took effect in 2014, roughly one in five Black Americans under 65 lacked coverage, compared with one in eight white Americans. Medical debt ravaged credit scores, blocked access to mortgages, and led to denials on car loans and small-business applications.

In countless interviews conducted at the time—and in the years since—the same themes emerged: emergency rooms used as primary care clinics, chronic diseases left unmanaged, children missing wellness visits because the cost of a single appointment could mean skipping rent.

The ACA aimed to change this architecture. And for a time, it did.

What the ACA Changed for Black Americans

The law began by widening the narrow doorway into Medicaid. For the first time, adults earning up to 138 percent of the federal poverty level—many working multiple jobs without benefits—were eligible for continuous coverage. Millions of Black adults who had spent years oscillating between emergency rooms and sliding-scale community clinics found themselves with insurance cards that offered access not only to acute care but to preventive services long out of reach.

Simultaneously, the ACA created an entirely new marketplace for people shut out of employer coverage. These online exchanges offered standardized plans and, crucially, federal subsidies that adjusted with income. For Black workers whose hours fluctuated with the season or whose employers relied on part-time schedules to avoid offering benefits, the marketplaces became a vital alternative.

The law also tore down some of the most discriminatory pillars of the insurance industry: bans on pre-existing condition exclusions, lifetime limits on benefits, and higher premiums for women. For Black families—who disproportionately experience chronic conditions like hypertension, diabetes, and asthma—these protections were especially profound.

The transformation was measurable. Between 2010 and 2022, the uninsured rate among Black Americans fell from about 21 percent to 11 percent. In states that expanded Medicaid, the gap in uninsured rates between Black and white adults narrowed significantly. Clinics in New Orleans and Detroit saw more patients arriving for preventive care rather than last-minute emergencies. Parents who had avoided doctor visits for years suddenly scheduled annual checkups. Chronic conditions that once went unmanaged began to stabilize.

For a single mother in Baton Rouge, the change meant she no longer had to choose between paying for insulin and paying for groceries. For a part-time substitute teacher on Chicago’s West Side, it meant finally controlling her blood pressure instead of visiting the emergency room every few months. The ACA didn’t eliminate racial health disparities—but it shifted the terrain.

A Pandemic Shock—and Lifeline

When COVID-19 struck, it laid bare long-standing inequities. Black communities saw higher infection rates, harsher economic fallout, and, in many cities, double or triple the mortality seen in white communities. Amid the trauma, the ACA provided an unexpected buffer.

Congress used the law’s existing structure to deliver a sweeping expansion of subsidies through the American Rescue Plan and later the Inflation Reduction Act. The enhancements increased financial assistance for low-income families, extended subsidies to many middle-income earners for the first time, and allowed millions of people to purchase plans with zero-dollar premiums.

For Black communities, the impact was immediate. Marketplace enrollment skyrocketed, with Black enrollment roughly tripling between 2020 and 2024. Stories poured in: a caterer in Detroit finally able to afford insulin; a home-health aide in Birmingham able to stay insured despite a modest pay raise; a gig worker in Houston who no longer feared a single medical bill would destroy his credit.

The subsidies were temporary by design, set to expire at the end of 2025. But they also revealed what a more equitable health system could look like when affordability was treated not as an aspirational goal but as a policy mandate.

Enter the One Big Beautiful Bill Act

The expiration date might have been manageable—if not for the One Big Beautiful Bill Act. On July 4, 2025, President Trump signed H.R. 1 into law, a sprawling legislative package that made permanent many of the 2017 tax cuts for corporations and high-income earners while balancing the budget through deep reductions in Medicaid and ACA-related spending.

The bill reshaped the safety net in ways both overt and subtle. It imposed nationwide work requirements for Medicaid, added copays for certain services, and reduced federal funding for the program—all changes that disproportionately affect Black workers, who are more likely to hold jobs with irregular schedules and unpredictable hours. By 2034, the Congressional Budget Office estimates that between 7.5 and 8 million people will lose Medicaid coverage as a result.

On the marketplace side, the law operates more like erosion than demolition. It allows the enhanced subsidies to expire without replacing them, a quiet but consequential omission. It eliminates automatic reenrollment—long a lifeline for low-income consumers juggling multiple jobs—and imposes new monthly fees on people who fail to reconfirm eligibility, even if they owe nothing. It narrows eligibility for lawfully present immigrants. It removes caps on repayment if incomes fluctuate, exposing low-wage workers to tax bills large enough to destabilize household budgets.

Taken together, these provisions threaten to undo much of the progress the ACA made for Black families.

How Black Communities Experience the Cuts

For many Black families, the return of high premiums and new administrative barriers feels like a reversion to an era they had hoped was behind them. Rising premiums push insurance just out of reach again; tighter Medicaid rules threaten to drop working adults from coverage if they miss a paperwork deadline; surprise tax bills loom for those whose income varies month to month.

In rural counties that are home to large Black populations, hospitals teeter on the edge of closure as Medicaid dollars recede. Maternity wards shutter, forcing Black mothers—already facing the nation’s highest maternal mortality rates—to travel hours for prenatal care or give birth in poorly equipped units. Clinics that once thrived on the stability the ACA brought now confront shrinking budgets and growing uncompensated care.

The administrative changes carry their own weight. The elimination of auto-renewal disproportionately affects people who work nights, care for aging parents, or lack reliable internet access. A missed email or a forgotten recertification appointment can now result in a loss of insurance—and with it, a cascade of financial damage: overdue medical bills, drops in credit scores, denials on car loans, evictions.

In the long view, these are not isolated setbacks. They reveal the reappearance of an old pattern: that when coverage becomes optional, unstable, or too expensive, the same communities that fought hardest for access fall first.

The Politics of a Vanishing Lifeline

In Washington, the battle over extending the enhanced subsidies has become a litmus test for the nation’s vision of health care. Democrats have introduced legislation to make the enhancements permanent and reverse the ACA-related cuts in the One Big Beautiful Bill. Republicans have countered that the subsidies are too costly, even as many of their constituents rely heavily on them.

Polling consistently shows that most Americans—across race and party—support keeping the subsidies in place. Yet political will remains elusive, leaving millions of families like Monique’s watching the calendar, trying to predict whether Congress will act before premiums reset.

Black advocacy organizations have framed the issue not only as a matter of coverage but of economic justice. The NAACP Legal Defense Fund describes the One Big Beautiful Bill as “the largest cut to safety-net programs in modern history,” arguing that it will “exacerbate racial inequities in health, wealth, and opportunity.” Their position echoes a broader truth: health care cannot be separated from financial stability. When Black families lose coverage, they lose bargaining power in every other domain—jobs, housing, credit, even education.

What Comes After the Safety Net?

Back in Atlanta, Monique closes her folder after her appointment. She now understands each scenario that hangs over her family: one where Congress renews the enhanced subsidies and her premium stays manageable, and one where it doesn’t—where she must choose which bill to delay to stay insured.

“I’m not trying to get something extra,” she says. “I’m just trying not to fall backward.”

The Affordable Care Act was never perfect. It was a compromise shaped by political limits and economic caution. But for fifteen years, it offered millions of Black families a measure of security they had rarely known. It lowered rates of uninsurance, reduced medical debt, and provided a buffer between illness and financial ruin.

The One Big Beautiful Bill Act does not erase that history. But it leans against it—gently, insistently, in ways that threaten to tip the balance back toward a health system where affordability is uncertain and coverage is conditional.

In the end, the future of Black health care in America may hinge not on sweeping court rulings or dramatic legislative showdowns, but on something quieter: a premium notice in a mailbox, a Medicaid recertification letter left unopened, a small hospital in a rural county closing its last labor and delivery unit.

For families like Monique’s, the question going forward is stark but familiar: how much protection does a nation owe those who have spent generations navigating its harshest edges? And what happens when even that protection begins to slip away?x