One of the earliest institutions meant to teach Black Americans how to save instead taught them how vulnerable they were to other people’s stewardship.

One of the earliest institutions meant to teach Black Americans how to save instead taught them how vulnerable they were to other people’s stewardship.

By KOLUMN Magazine

There is a particular burden placed on Black-owned banks in the American imagination. They are expected to be practical and symbolic, solvent and visionary, conservative enough to survive and radical enough to matter. They are asked to finance homes, churches, funeral homes, beauty salons, contractors, first-generation entrepreneurs, and the neighborhood institutions that rarely make national headlines but often determine whether a community feels stable or exposed. They are also expected to carry memory. In them lives the story of exclusion, the discipline of mutual aid, the promise of self-determination, and the persistent belief that money, if gathered and circulated with intention, can become something larger than currency. It can become infrastructure. It can become leverage. It can become time.

To write about Black-owned banks is to write about American democracy in one of its clearest material forms: who gets credit, on what terms, under whose supervision, with what assumptions, and with how much room for error. Banking is often narrated as technical machinery, a matter of rates, reserves, regulation, and branch footprints. But in Black America, banking has never been merely technical. It has always been social and political. A mortgage denial is a civic fact. A business loan approval is a neighborhood event. A bank branch in a Black commercial corridor is not just a storefront with tellers and forms; it is a declaration that a community is legible to finance and worthy of institutional permanence.

Black-owned banks emerged because the American financial system was not colorblind. They were built because exclusion was routine, discrimination was profitable, and access to credit was distributed along racial lines for generations. The need was not abstract. Newly emancipated people needed places to save wages. Black workers needed institutions that would take their money seriously. Black entrepreneurs needed lenders who could see possibility where mainstream banks saw only risk. Black families needed somewhere to put their earnings without being forced to rely on institutions that had either shut them out or welcomed them on hostile terms.

The history of Black-owned banks is therefore not a side story in American finance. It is one of the main stories. It reveals how Black communities built institutions under pressure, how those institutions were constrained by the very inequalities they were supposed to help overcome, and why the question of who controls capital inside Black neighborhoods remains unresolved even now. As of February 2026, Forbes counted 24 Black-owned banks operating as official minority depository institutions, a small number relative to the scale of Black America and the historical role these institutions have played. Their numerical modesty makes their endurance more striking, not less.

A Bank for Freedom, A Lesson in Loss

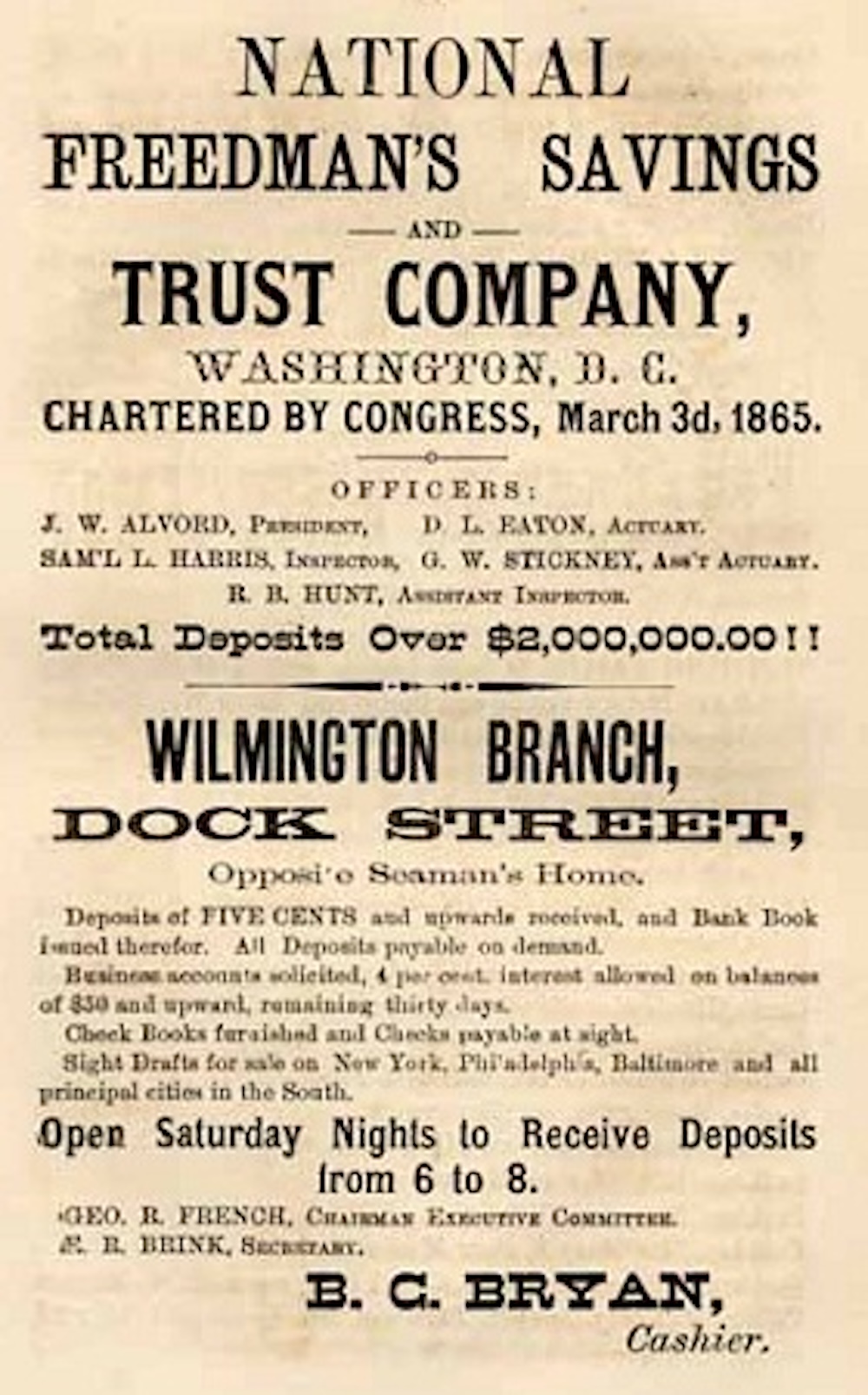

The first chapter in this story is not triumph, but betrayal. In 1865, Congress chartered the Freedman’s Savings and Trust Company in the same broad Reconstruction moment that produced the Freedmen’s Bureau. The bank was designed to help newly emancipated Black Americans enter financial life. Formerly enslaved people, Black Union soldiers, laborers, teachers, and domestic workers could deposit wages and begin the difficult work of building economic security in a nation that had only recently stopped treating them as property. The institution’s very existence suggested that financial participation would be part of freedom’s practical meaning.

But the promise was compromised almost from the beginning. The Office of the Comptroller of the Currency notes that despite its congressional charter, the bank was not supervised by the OCC the way national banks were. It lacked the kind of regulatory discipline that might have kept it from drifting into dangerous real-estate lending and speculative practices. Oversight was episodic. Political influence was heavy. Governance deteriorated. By the time Frederick Douglass was brought in as president in March 1874 in a last effort to reassure depositors, the institution was already effectively unsalvageable. On June 29, 1874, the trustees voted to close it. More than 61,000 depositors were left with losses of nearly $3 million, and many ultimately recovered only part of what they had entrusted to the bank.

The first great Black banking story in America was not simply a failure of finance. It was a failure of stewardship.

The collapse of Freedman’s Bank mattered far beyond the ledgers. It taught an early and brutal lesson: a federal charter did not mean federal protection, and formal inclusion could still end in devastation. For Black depositors, many of whom were only beginning to accumulate wages and savings, this was not the loss of discretionary wealth. It was the loss of first wealth, fragile wealth, freedom’s first cash value. The St. Louis Fed notes that distrust of financial institutions in Black communities is often traced, in part, to this collapse. That distrust was not irrational. It was historically produced.

The Founding and Collapse of Freedman’s Savings and Trust Company

Freedman’s Savings and Trust Company is often described as the beginning of Black banking in the United States, though that description can be slightly misleading. It was not Black-owned in the later sense of the term. It was instead an institution created for Black depositors during Reconstruction, governed largely by white trustees, and closely associated in the public imagination with federal authority. That distinction matters because it explains both the scale of trust the bank inspired and the depth of injury when it failed.

Its founding rested on a compelling idea. Newly freed people needed a secure mechanism for savings, and the transition from enslavement to paid labor required financial institutions that could receive deposits, record balances, and symbolize a new kind of civic standing. The bank expanded rapidly through branches across Southern states and major cities, drawing depositors who often believed their money was guaranteed by the government. But that trust was built on a misunderstanding. The OCC has been explicit: Freedman’s was not subject to the same supervisory framework as national banks, and the absence of rigorous examination helped clear the path for bad lending and political favoritism.

Its collapse was equally instructive. The bank’s failure was caused not by some moral deficiency among its depositors, but by managerial decisions, weak oversight, and structural carelessness. The result was a civic trauma. In Black financial history, Freedman’s Bank became a warning about the distance between symbolic recognition and actual protection. It is one reason later Black-owned banks placed such weight on local trust, governance discipline, and leadership that was answerable to the community rather than imposed from outside.

Building Institutions From Within

If Freedman’s represented the danger of dependence on outside stewardship, the next phase of Black banking represented something more self-determined. In the late 19th century, Black communities built financial institutions from within networks they already trusted: churches, mutual-aid societies, benevolent associations, and fraternal orders. These organizations had long handled sickness benefits, burial funds, social support, and collective discipline. Banking became a natural extension of that world. It was not yet finance as elite abstraction. It was finance as organized survival.

The Kansas City Fed’s historical work on the founding of America’s first Black banks emphasizes that these institutions did much more than take deposits. They offered training, jobs, and local credit. They were community banks in the deepest sense, rooted in neighborhoods and accountable to people whose lives were visible to them. In a segregated society, that visibility mattered. A Black banker in a Black commercial district understood local reputation, church ties, family history, and the difference between precariousness and irresponsibility. Those are forms of information that rarely show up neatly in national credit models.

This is also where the mythology of “self-help” has to be handled carefully. Black institution-building was real and remarkable, but it did not happen on an even field. These banks were trying to create circulation in communities systematically denied opportunities to accumulate capital at scale. They were not building under merely competitive conditions; they were building under conditions of extraction. That is why their existence was so impressive and why their balance sheets were often so strained. A bank can help mobilize wealth. It cannot simply invent wealth that public policy and private discrimination have spent decades suppressing.

The Founding and Collapse of the Grand Fountain of the United Order of True Reformers

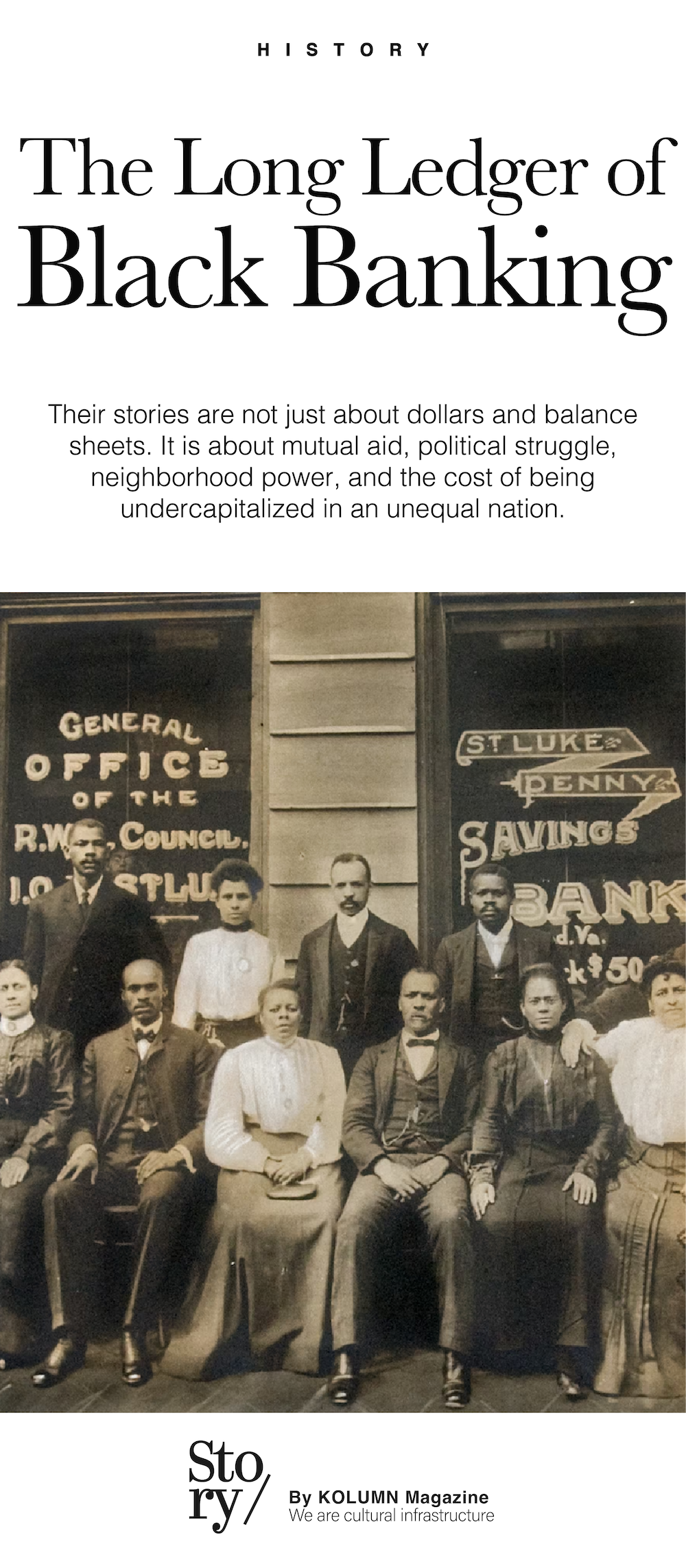

One of the most important institutions in this next chapter was the Savings Bank of the Grand Fountain of the United Order of True Reformers in Richmond, Virginia. According to Encyclopedia Virginia, the bank was created by an act of the General Assembly on March 2, 1888, making it the first Black-owned, Black-operated financial institution chartered in the United States. It emerged from a larger fraternal order that already provided insurance and mutual aid, and under the leadership of William Washington Browne it became part of a remarkably ambitious Black enterprise ecosystem.

The bank’s founding was not a narrow banking event. It was an institutional strategy. The True Reformers created a multipurpose building in Richmond that housed the bank, business offices, stores, meeting rooms, and a concert hall. They later expanded into publishing, real estate, and hospitality, including the now-famous True Reformer building in Washington, D.C. The organization demonstrated a central truth of Black economic history: communities denied full access to mainstream systems often build parallel infrastructures that are not merely substitutes, but laboratories of ambition.

The True Reformers were not just collecting deposits. They were constructing an ecosystem.

But the True Reformers’ story also reveals how vulnerable such ecosystems could be. After Browne’s death in 1897, leadership continuity weakened. And in October 1910, the Virginia State Corporation Commission closed the bank after a member was caught embezzling more than $50,000 from member deposits, while several businesses defaulted on large unsecured loans the bank could not cover. The institution’s collapse was not simply a morality play about one bad actor. It was a lesson in the importance of internal controls, governance succession, and capitalization. Vision had built the enterprise. Systems were not strong enough to preserve it.

Still, the True Reformers’ significance did not end when the bank did. Their example traveled. The Library of Congress noted in 2025 that the True Reformers served as a model for later efforts, including those associated with Maggie Lena Walker. That matters because Black banking history is not just a list of isolated institutions. It is a chain of inheritance. One bank’s design, even if it fails, can become another generation’s starting point.

Maggie Lena Walker and the Discipline of Institution-Building

Few figures embody that inheritance more clearly than Maggie Lena Walker. She remains rightly famous as the first Black woman in the United States to charter and serve as president of a bank, but the title can undersell the breadth of what she built. Walker understood banking not as a stand-alone business but as one element in a larger program of racial advancement. Through the Independent Order of St. Luke, she tied together finance, media, retail, and mutual support into a coherent institutional philosophy. A bank, for Walker, was not merely a place to store money. It was a school of discipline, a mechanism of confidence, and an emblem of Black managerial authority.

The National Park Service notes that at the 1901 annual convention of the Independent Order of St. Luke, Walker laid out goals that included a bank, an emporium, a newspaper, and a factory. That planning reveals how deliberately she thought about economic power. She did not imagine finance as disconnected from commerce or public voice. She imagined a full civic architecture, one in which a Black institution could underwrite Black livelihoods and normalize Black expertise at the highest levels of financial administration.

Walker’s importance also lies in the tone of her model. Where some earlier ventures were expansive and vulnerable to overreach, St. Luke’s banking culture leaned toward disciplined thrift. Small deposits mattered. Professionalism mattered. Transparency mattered. There was grandeur in the vision, but there was also method. That blend helps explain why the institution she founded proved so consequential.

The Founding and Transformation of St. Luke Penny Savings Bank

St. Luke Penny Savings Bank was founded in 1903 in Richmond, Virginia, out of Walker’s leadership of the Independent Order of St. Luke. The National Park Service explains that Walker saw the bank as a way to combat segregation while encouraging thrift and economic independence in the Black community. The institution welcomed small deposits from working people, converting pennies into participation and participation into capital. Its very name signaled a theory of change: no deposit was too modest to matter if enough people believed in the institution receiving it.

Unlike Freedman’s Bank, this institution was not defined by outside management. Unlike the True Reformers, it became associated with a highly visible model of disciplined leadership and strategic adaptation. The St. Luke bank was part of a broader ecosystem that included commercial ventures and media, but it did not rely on spectacle. It relied on steadiness. The Library of Congress notes that Walker’s achievement made her the first African American woman to establish a bank in the United States, a distinction that mattered not only for representation but for the normalization of Black women’s financial authority in public life.

Its story of “collapse” is more complicated than those of Freedman’s and the True Reformers because St. Luke Penny Savings Bank did not simply implode and disappear. Rather, it evolved. Encyclopedia Virginia notes that after the 1910 embezzlement scandal involving the True Reformers’ bank, Virginia required fraternal societies and financial institutions to be legally separate. Later, during the pressures of the Great Depression, Walker helped guide a merger of Richmond’s Black banks into Consolidated Bank and Trust Company in 1930. The National Park Service notes that Walker then served as chairman of the board. In other words, St. Luke did not end in disgrace; it transformed in order to survive.

Maggie Lena Walker’s great financial insight was that ambition without structure is not liberation. It is exposure.

That distinction matters. In Black banking history, survival has often required structural evolution. Mergers, reorganizations, and legal separation were not necessarily defeats. They were sometimes the price of durability. St. Luke’s legacy lies not only in its founding, but in the fact that its mission continued through adaptation rather than ending in collapse. That makes it one of the most important early examples of Black financial institution-building done with enough rigor to outlast a founding moment.

The Geography of Exclusion

By the early 20th century, Black-owned banks had become critical components of Black commercial life in places like Richmond, Durham, Atlanta, and beyond. They were part of the architecture of Black business districts, helping finance property purchases, small enterprises, and local organizations. But their operating environment remained punishing. The problem was never just whether a bank existed. It was the geography around it: which neighborhoods were considered investable, which households had been allowed to build wealth, and which business corridors were starved of credit.

The Federal Reserve’s history of redlining makes clear how race and place were fused in American lending. Redlining denied credit based on neighborhood composition, especially in Black urban neighborhoods, even when individual borrowers were qualified. The Fair Housing Act of 1968 outlawed racially motivated redlining, but a ban on explicit discrimination did not undo the decades of suppressed home values, weak tax bases, and reduced intergenerational wealth that redlining produced. Black banks did not operate outside that damage. They inherited it.

This helps explain one of the structural dilemmas of Black-owned banks. They often serve communities with greater need and fewer accumulated buffers. Their borrowers may be stronger than the data suggests in terms of reputation, resilience, and informal support, but weaker on the paper metrics financial markets have historically favored. Relationship banking can partially bridge that gap. It cannot erase the legacy of policy-driven disinvestment.

What Black-Owned Banks Actually Do

The St. Louis Fed has argued that Black-owned banks have consistently maintained their focus on Black-owned small firms, nonprofits, and Black families, and that their branches serve majority-Black areas that have often been hit especially hard by economic shocks. The FDIC’s research on minority depository institutions similarly found that MDIs originate a greater share of mortgages in low- and moderate-income census tracts and in tracts with larger minority populations than non-MDIs, and that they play a disproportionate role in SBA lending in those places. Those findings get closer to the real point. The significance of Black-owned banks is not captured simply by counting how many exist. It is captured by what kinds of communities they keep showing up for.

This is why symbolic language can sometimes obscure more than it reveals. A Black-owned bank is not valuable only because it signifies self-determination. It is valuable because it underwrites payroll. Because it can finance a church expansion, a corner commercial building, or a family’s first mortgage. Because it may know the borrower beyond an algorithmic score. Because in places where branch access has thinned and mainstream financial trust remains shallow, it can still function as a civic institution rather than a distant platform.

The Arithmetic Problem

And yet sentiment cannot repeal arithmetic. Black-owned banks have always been asked to solve inequality while operating within it. They tend to be smaller than the national giants they compete with. Their deposit bases are often thinner. Their compliance burdens are real. Their technology needs are expensive. Their customers are frequently navigating the downstream effects of discrimination in housing, labor, and capital markets. This is why the romantic version of Black banking can become unfair. It asks institutions built under constraint to perform miracles.

Brookings has documented some of the barriers surrounding Black entrepreneurship and finance. In 2021, just 13 percent of Black-owned businesses were likely to receive the financing they applied for, compared with 40 percent of white-owned businesses. A New York Fed release on the Small Business Credit Survey reported the same broad disparity, noting that 46 percent of Black-owned firms that applied for financing received none of what they sought. Those figures show why Black-owned banks matter, but they also show why they cannot carry the entire burden alone. A small set of community institutions cannot, by themselves, close a national financing gap built over generations.

Decline, Consolidation, and the Modern Squeeze

The number of Black-owned banks declined substantially over the late 20th and early 21st centuries. The FDIC’s MDI research found that African American MDIs fell by more than half between 2001 and 2018. Some of this reflected consolidation. Some reflected succession problems, scale challenges, and competitive pressure from much larger banks. Some reflected the paradox of post-civil-rights inclusion: once mainstream institutions were more present in Black communities, Black-owned banks had to compete against firms with much deeper balance sheets and technological reach. Progress in access did not automatically produce strength in Black ownership.

The Great Recession intensified those pressures. Black households were disproportionately harmed by predatory subprime lending and the foreclosure crisis. Communities already carrying the long afterlife of redlining were hit again. In that setting, Black-owned banks gained renewed importance as institutions that had reason to understand the difference between fair lending and exploitative inclusion. But they, too, were operating in a battered environment. The borrowers most in need of patient credit were often those whom the crisis had damaged most severely.

From #BankBlack to the Present

The modern #BankBlack movement gave the sector new public visibility. Calls to move deposits into Black-owned institutions intensified after public acts of racial violence and renewed national debates about structural inequality. This visibility did not solve the sector’s challenges, but it did remind a broader public that where money rests is also a civic question. Black-owned banks were recast not as historical curiosities, but as live institutions connected to current debates over racial wealth, community investment, and economic agency.

After 2020, larger financial institutions and federal policymakers also increased support for minority-focused lenders. Reuters reported in 2023 that minority-owned banks weathered industry turmoil in part because of government and industry support. That same year, Reuters also reported on Biden administration efforts to spur an additional $2 billion in corporate deposits into community lenders serving minority and underserved businesses, alongside procurement goals meant to strengthen the broader ecosystem around them. Those moves matter because deposits and capital support lending capacity, staffing, and technological modernization. Praise does not update a core banking system. Capital does.

There is, however, a tension built into this new phase. Support from larger institutions can help stabilize Black-owned banks, but it can also leave them dependent on arrangements shaped elsewhere. The fundamental question remains the same as it was a century ago: are Black-owned banks being recognized as permanent financial actors with the scale to grow, or as worthy symbolic partners whose survival depends on periodic external rescue? The answer is uneven. Some institutions have leveraged new partnerships to improve staffing and digital services. But the deeper issue of long-horizon capitalization remains unresolved.

Small in Number, Large in Meaning

Today’s Black-owned banks remain few in number, but that scarcity should not invite sentimental overstatement or dismissive underestimation. They are not relics. They are specialized institutions performing work that many larger firms have not done consistently or well in Black communities. They are also evidence of a long tradition of Black institutional competence, one that is too often spoken of in commemorative language rather than funded with seriousness.

One reason these banks endure in public meaning is that they preserve a record of Black communities doing more than merely surviving exclusion. They built systems. They hired clerks and officers. They taught practices of thrift and credit. They financed buildings and payrolls. They made expertise reproducible. The founders of the True Reformers, the depositors of Freedman’s Bank, and Maggie Lena Walker were not all engaged in the same kind of project, but they were all confronting a common question: how does a people denied equal standing build durable institutions anyway?

The Future of Black Banking

The future of Black-owned banks will likely depend on whether they can hold together three things at once. The first is trust, the historical advantage that comes from mission, local knowledge, and community accountability. The second is digital competence, because banking now happens as much on screens as in branches, and small institutions cannot ask customers to choose between solidarity and convenience. The third is capitalization sufficient to lend through downturns rather than retreat during them. Without that third element, every crisis risks shrinking the very institutions communities most need to remain steady.

This is why the strongest case for Black-owned banks is not romantic but structural. They should not be understood merely as symbolic beneficiaries of goodwill campaigns. They are part of the country’s community-finance infrastructure. If the United States is serious about expanding fair access to credit, reducing branch deserts, and supporting Black business formation, then Black-owned banks and other mission-driven minority institutions belong inside that strategy, not at its decorative edge.

More Than a Place to Deposit Money

In the end, the history of Black-owned banks is larger than banking. It is about the effort to turn money into freedom and then defend that freedom against mismanagement, discrimination, market concentration, and policy neglect. Freedman’s Savings and Trust Company showed how devastating it is when trust is solicited without protection. The Grand Fountain of the United Order of True Reformers showed how bold Black institution-building could be, and how governance failures could undo even a visionary ecosystem. St. Luke Penny Savings Bank showed that disciplined leadership, small deposits, and structural adaptation could produce something rarer: endurance.

The long ledger of Black banking is therefore not a simple story of rise and fall. It is a story of repeated attempts to claim agency in a financial system that has often assigned Black communities the role of customer without control, borrower without leverage, neighborhood without investment. Black-owned banks have insisted on something more ambitious: ownership, intermediation, and continuity. In American history, that has never been a small demand. It has often been the difference between wealth that circulates locally and wealth that leaks away, between development that answers to a neighborhood and development done to it.

That is why these institutions still matter. Not because they are nostalgic symbols of a lost era, but because they remain active arguments about power. Who decides what counts as risk. Who gets to translate savings into security. Who gets to recognize value before the rest of the market does. Black-owned banks have been answering those questions for more than a century, sometimes with grand institutions, sometimes with modest branches, sometimes with a balance sheet far too small for the burden history placed on it. Their significance lies in the fact that they kept answering anyway.

More great stories

The Schoolmaster of Freedom

March 18, 2026

No Comments

Before Detroit, There Was Greenfield

March 18, 2026

No Comments