The

Vanishing Lifeline

How a congressional stalemate is pushing millions of Americans toward a health-care cliff

By KOLUMN Magazine

Congress as the Center of the Storm

In Washington, the final weeks of the legislative calendar have been consumed by a fight over the future of the Affordable Care Act’s enhanced subsidies—temporary provisions that, for four years, have kept premiums historically low for millions of Americans. Congress entered the winter session facing the same decision it has postponed for more than a year: whether to extend the expanded tax credits enacted during the pandemic, allow them to expire at the end of 2025, or replace them with a narrower, more ideologically driven alternative.

That decision has become one of the most consequential unresolved questions in federal health policy. In early December, the Senate failed to advance competing bills—one Democratic proposal to extend the enhanced subsidies for three additional years, and a Republican alternative built around health savings accounts and one-time direct payments. The House, meanwhile, has splintered into bipartisan factions promoting short-term extensions, a leadership bloc advocating for more restricted reforms, and a pair of discharge petitions too late-arriving to influence the 2025 enrollment cycle.

As lawmakers traded amendments and floor speeches, the Congressional Budget Office issued projections warning that the expiration of the enhanced credits would trigger steep premium spikes starting in 2026, potentially pricing out millions of households. Governors, marketplace administrators, and hospital systems urged Congress to act, pointing to fragile post-pandemic insurance gains and rising uncompensated care costs.

But Congress adjourned without a resolution—leaving states, insurers, and families with no clear guidance as they prepare for a fundamentally altered health-care landscape. For residents in states most dependent on ACA subsidies, the consequences of federal paralysis are already reflected in projected 2026 premiums. Families who had come to rely on the enhanced credits as a stable fixture of the national safety net are now confronting the reality that the policy was temporary all along, and its survival rests on a Congress increasingly unable to agree on how—or whether—to sustain the Affordable Care Act framework that has defined coverage for a decade.

And across the country, in clinics, community centers, and kitchen-table budgeting sessions, the political gridlock in Washington is becoming a household emergency.

How a Temporary Patch Became a Lifeline

The Affordable Care Act has always been powered by subsidies. When the law took effect in 2014, premium tax credits were its central promise: a guarantee that people shut out of employer insurance could buy coverage on the marketplace at a cost tied to their income.

But the subsidies now in jeopardy are not those foundational credits. They are the “enhanced” subsidies—temporary increases passed in the 2021 American Rescue Plan and later extended through 2025 by the Inflation Reduction Act.

These changes:

* Raised the value of existing subsidies.

* Capped premiums at 8.5 percent of a household’s income.

* Eliminated the infamous “subsidy cliff,” extending help to many middle-income families for the first time.

The results were immediate. Marketplace enrollment surged to more than 24 million people, an all-time high. The uninsured rate dropped to record lows. And the political map shifted: the majority of marketplace enrollees now live in states that Donald Trump won, especially in the South and Mountain West—regions that declined to expand Medicaid and where ACA subsidies play an outsized role.

In those states, the enhanced credits often rendered benchmark silver plans free for low-income adults—effectively substituting for Medicaid in places where local governments refused to broaden eligibility.

The temporary fix, in short, became a structural pillar.

The 2026 Cliff

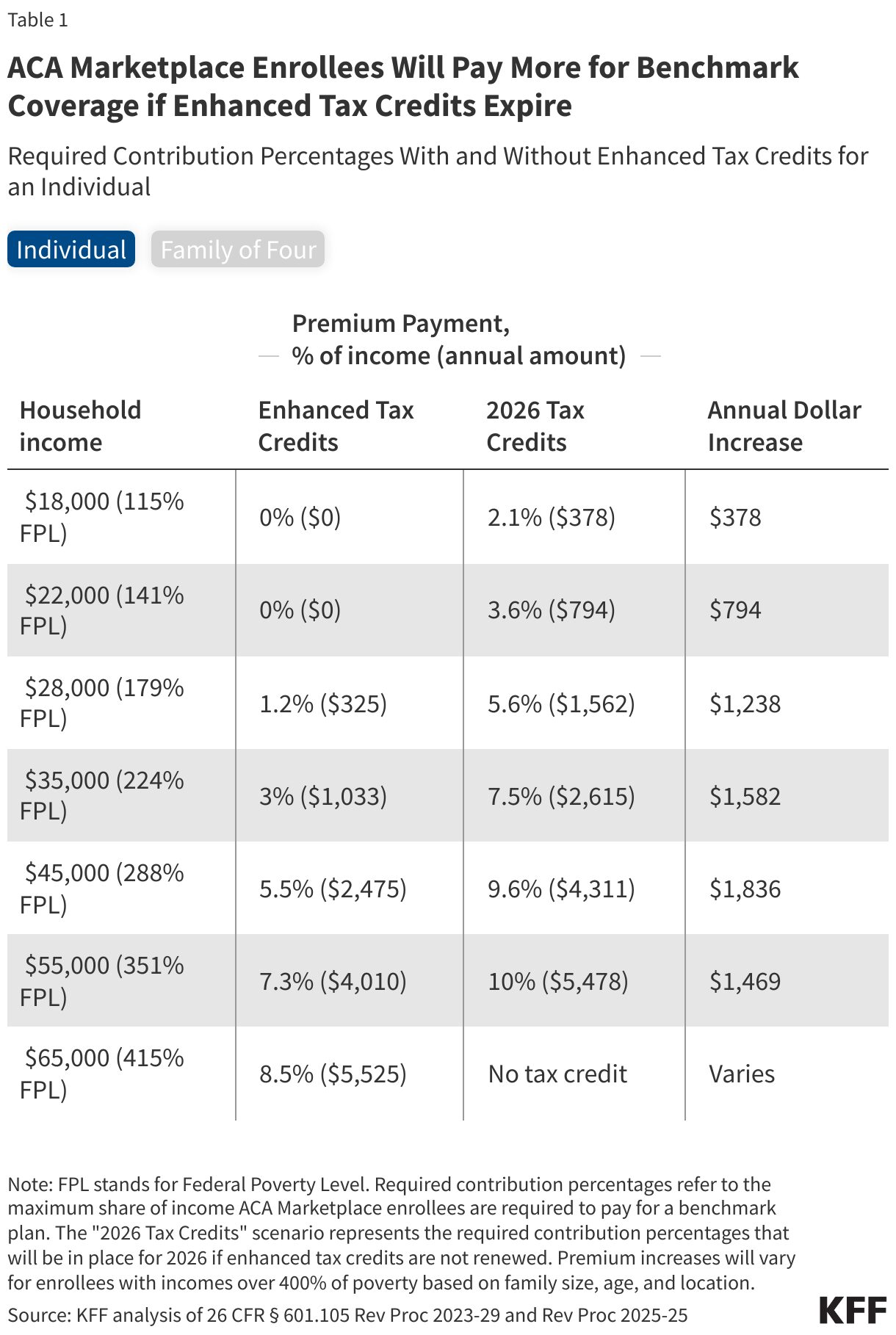

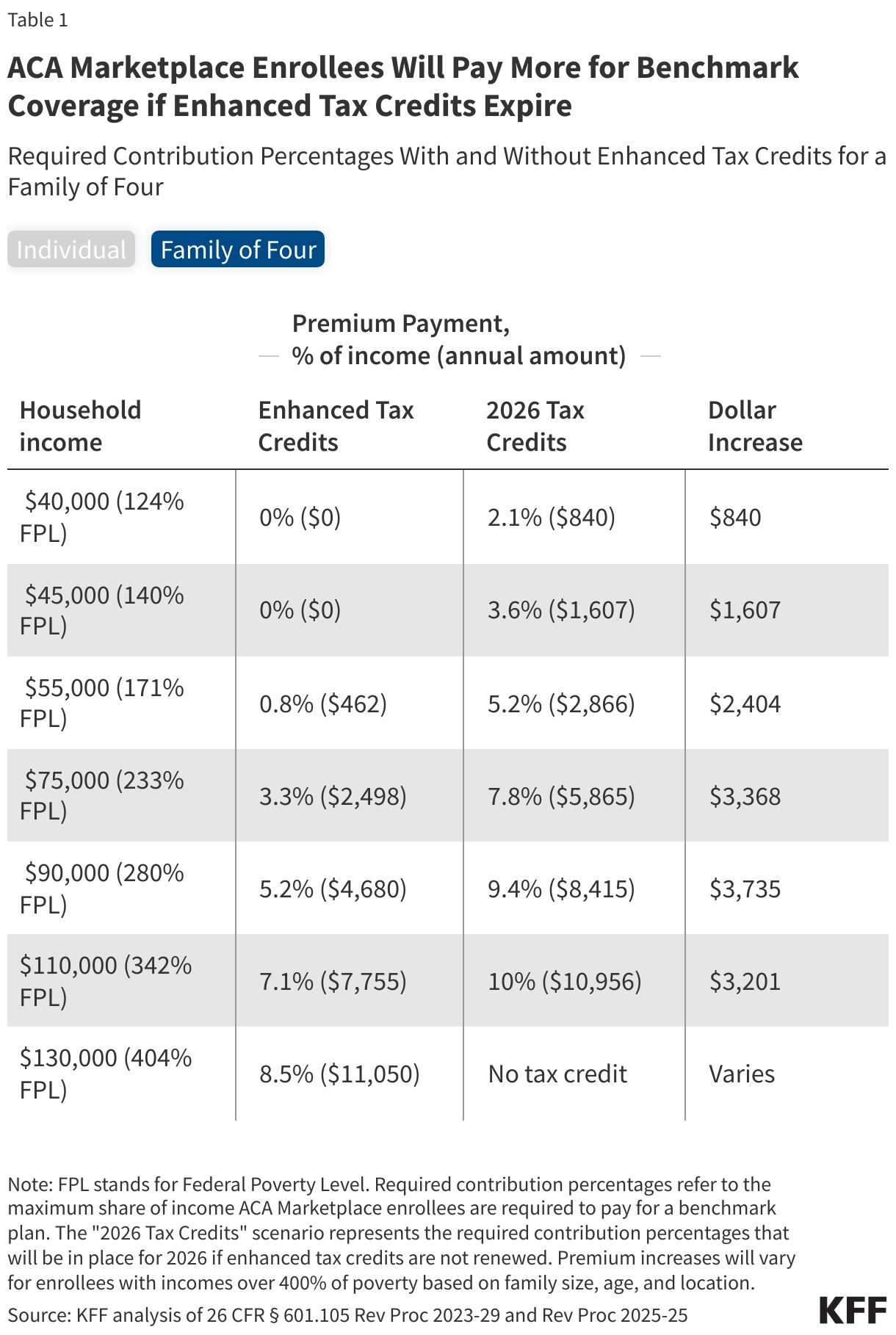

If Congress does not act, the enhanced credits vanish on December 31, 2025.

Premiums will not merely rise; they will snap back to pre-pandemic formulas. The subsidy cliff returns. Middle-income families in high-premium markets lose assistance altogether. Lower-income families must once again contribute a higher share of their income toward coverage.

Independent estimates are stark:

* Average premium payments more than double in 2026, rising 114 percent.

* Four to five million Americans could lose coverage outright.

* Deductibles and out-of-pocket exposure will rise as families downgrade to cheaper bronze plans.

And the budgeting thresholds are unforgiving. Surveys show more than half of ACA enrollees could not afford even a $300 increase in annual health costs. The typical projected jump in 2026 is several times that amount.

When a Political Crisis Becomes a Household Emergency

If the debate in Washington is abstract, the stakes at home are anything but.

In Atlanta, a mortgage underwriter named Monique sits at a community health center with a folder of renewal documents. For four years, the enhanced subsidies kept her family’s silver plan at a manageable $90 a month. Her sons have asthma; the plan covers their inhalers and specialists. Without an extension, her premiums more than double.

“I approve mortgages for people ruined by medical bills,” she says. “Now I’m wondering if that’s going to be us.”

In Chicago, 34-year-old education consultant Daniela Perez is delaying enrollment altogether. Her premium could climb from $180 to more than $1,200 a month without the enhanced credit. “Every plan feels like a temporary plan,” she tells a navigator. “Congress is too gridlocked to bank on anything.”

In Southern California, Debra Nweke and her husband face a leap from $1,000 to $2,400 a month. “How can insurance cost more than rent?” she asks.

And in rural Texas, Andrew Schwarz—a preacher and gig worker—faces a modest-sounding jump from $40 to $150 a month. But that $110 difference is the margin between paying the light bill and putting off care.

These stories reflect a broader reality: families are being forced to make health and financial choices based on what Congress did not do.

States That Live and Die by the Subsidy

The impacts of subsidy expiration are geographically uneven.

The steepest projected increases hit:

Wyoming, West Virginia, Alaska – annual premium jumps of $19,000–$22,000 for older enrollees just above the subsidy cliff.

Non-expansion states – where ACA plans effectively function as Medicaid for low-income adults, out-of-pocket costs could rise 77 to 195 percent.

California – nearly two million residents could see premiums double; up to 400,000 could be priced out.

Texas’s 15th Congressional District—represented by Republican Monica De La Cruz—has one of the nation’s highest marketplace enrollment rates. For a 60-year-old couple earning $82,000, premiums could triple under the old subsidy formula.

The irony is difficult to miss: many of the states most critical of the ACA now rely on its subsidies the most.

How Subsidy Cuts Reopen Racial Fault Lines

The ACA was one of the most effective tools ever deployed to narrow racial gaps in health coverage. Before it passed, roughly one in five Black adults lacked health insurance. After its implementation, that rate fell sharply.

Enhanced subsidies accelerated the gains. Black families reported shifts from sporadic care to stable primary care, from emergency room visits to routine management of chronic conditions.

Those gains are now at risk.

The expiration of enhanced subsidies and the accompanying tightening of Medicaid eligibility threaten to widen racial disparities once again. Black households, which devote a higher share of income to housing, food, and debt, are more vulnerable to even modest increases in health premiums. Analysts warn that millions of Black and Latino enrollees could be pushed into the ranks of the uninsured if Congress allows the subsidies to expire.

In Monique’s Atlanta clinic, the burden is visible: workers with unstable schedules, caregivers juggling multiple jobs, and patients who lose coverage over a missed recertification email. Without the enhanced credits, they become the shock absorbers of federal inaction.

The Argument for—and Against—Extending the Subsidies

Public sentiment is lopsided: 78 percent of Americans say Congress should extend the enhanced subsidies. Support is bipartisan.

The arguments for extension are practical:

* The enhanced credits stabilized the individual market.

* They reduced the uninsured rate to its lowest point in history.

* They prevented medical debt spikes and hospital uncompensated-care crises.

* They function as immediate, direct affordability relief—not a deferred tax benefit.

Opponents, chiefly conservative policy groups and Republican budget chairs, argue:

* Enhanced subsidies distort insurance markets by masking true premium growth.

* They benefit households that could otherwise absorb higher costs.

* They represent an “unsustainable” long-term federal expenditure.

Democrats counter that the alternatives—chiefly HSA-centered plans—are unusable for low-income families who can’t front the cost of premiums or deductibles.

The impasse has solidified. Neither the Democratic nor Republican proposal cleared the Senate. The House remains scattered.

If Congress Fails to Act

Should Congress continue its stalemate, the effects will unfold in phases:

Premium shock – the immediate doubling of costs for millions.

Plan downgrades – a shift to bronze plans with deductibles exceeding $7,400, making meaningful access nearly impossible.

Coverage drops – millions losing insurance altogether.

Systemic strain – rural hospitals destabilized, community clinics overwhelmed, medical debt rising sharply.

For families, the sequence translates to postponed care, skipped medications, and the return of medical bankruptcy as a defining American risk.

A Country at a Crossroads

The Affordable Care Act has never been static. It has survived repeal attempts, Supreme Court cases, shifting congressional majorities, and the turbulence of national politics. But the fate of its enhanced subsidies may prove its most consequential test yet.

The question before Congress is simple: Should health insurance for millions remain affordable? But the effects of their inaction are anything but simple. They reverberate through workplaces, budgets, hospitals, and the households of people for whom health insurance is not an ideological abstraction but a monthly line item with life-and-death implications.

Back in Atlanta, Monique leaves the clinic with two numbers circled on her printout: what she pays if Congress acts, and what she pays if it does not. She follows news alerts on her phone—the failed votes, the stalled negotiations, the promises of future cooperation.

“To them, it’s politics,” she says. “To us, it’s whether my kids get to see their asthma doctor next year.”

Her calculation—and millions like hers—now defines the true cost of congressional inaction.